AI 公司美股 IPO 定價思維的結構性演變——從技術敘事回歸實體約束

AI 公司美股 IPO 定價思維的結構性演變——從技術敘事回歸實體約束

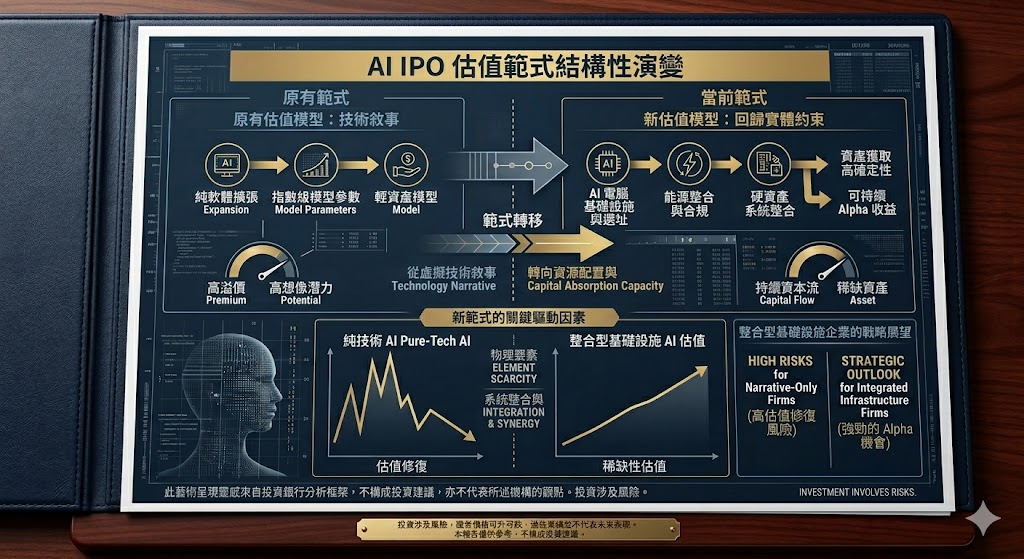

當前美國資本市場對於 AI 相關企業的評價體系正經歷一場深度的範式轉移。投資者的定價邏輯已正式告別純粹的「技術想像力」階段,轉而聚焦於企業解決實體世界硬性約束的確定性。這一轉變不僅定義了新一代 AI 基礎設施企業的估值底色,更預示著資本對於 AI 產業鏈價值的重新分配。

市場分析:要素稀缺性下的估值重構

在過去的市場週期中,軟體擴張的「輕資產」模式與模型參數的「指數成長」是獲取高溢價的核心。然而,隨著 AI 算力需求的爆炸式成長觸及物理邊界,資本市場的定價天平開始向具備系統性交付能力的「硬資產」傾斜:

物理約束的資產化: 市場已意識到,AI 訓練與推理的瓶頸不再僅限於演算法,而是受限於電力獲取、用地審批及合規的能源供應。具備獲取這些底層要素能力的企業,實質上掌握了 AI 增長的「准入門檻」。這種從虛擬技術向物理資源約束的轉向,使資源整合能力成為估值的核心變量。

系統集成與協同溢價: 單一技術或能源解決方案在面對複雜的 AI 負載時,其風險分散與成本控制能力已顯不足。能夠橫跨核能、天然氣、可再生能源及儲能技術,並將其轉化為穩定、低成本電力輸出的「系統級供應商」,展現出更強的利潤韌性。這種系統級的組合能力,正成為對標傳統基礎設施企業時獲得超額收益(Alpha)的關鍵。

長週期資本的護城河: 過去被視為負擔的重資產、長週期開發模式,在當前環境下被重新定義為「稀缺性」。大規模數據中心與能源配套設施的建設需要極高的資本門檻與跨週期執行力,這類企業通過公開市場承接大規模長期資本,構建了難以被模仿的競爭壁壘,從而實現了從「故事導向」向「資產承載力導向」的估值躍遷。

風險與展望:回歸底層邏輯的戰略選擇

近期如 Arm、Astera Labs 等企業的市場表現,均驗證了資本對於「解決真問題」企業的強烈偏好。對於後續擬進行首次公開發行(IPO)的企業而言,依賴單一 AI 標籤的時代已宣告結束。

戰略展望: 企業需審視其是否具備處理底層物理約束的能力,以及是否能將複雜的資源轉化為系統化的交付方案。未來,具備大規模資本承載力且能提供確定性產出的企業,將在波動的宏觀環境中持續獲得市場青睞。反之,缺乏實體支撐的純技術敘事,將在估值修復的過程中面臨嚴峻的流動性與定價考驗。

投資涉及風險,證券價格可升可跌,過往業績並不代表未來表現。本報告僅供參考,不構成投資建議。

The Structural Evolution of AI IPO Valuation: From Technical Narrative to Physical Constraints

The valuation framework for AI-related enterprises in U.S. capital markets is undergoing a profound paradigm shift. Investor pricing logic has officially moved beyond the phase of "speculative technical imagination," pivoting instead toward the certainty of a company’s ability to resolve real-world physical bottlenecks. This transition not only redefines the valuation floor for next-generation AI infrastructure but also signals a fundamental reallocation of capital across the AI value chain.

Market Analysis: Revaluation Under Factor Scarcity

In previous cycles, the "asset-light" software expansion model and the "exponential growth" of model parameters were the primary drivers of premium valuations. However, as the explosive demand for AI compute hits physical boundaries, the pricing scales are tipping toward "hard assets" with systemic delivery capabilities:

Financialization of Physical Constraints: Markets now recognize that bottlenecks in AI training and inference extend beyond algorithms to power procurement, land use permits, and compliant energy supply. Companies capable of securing these foundational inputs effectively control the "barrier to entry" for AI growth. This shift from virtual narratives to physical resource mastery makes resource integration capability a core valuation variable.

Systemic Integration & Synergy Premiums: Isolated technology or energy solutions are increasingly inadequate for managing complex AI workloads due to insufficient risk diversification and cost control. "System-level providers"—those capable of bridging nuclear, natural gas, renewables, and storage to deliver stable, low-cost power—demonstrate superior earnings resilience. This holistic orchestration is becoming the key to generating Alpha when benchmarked against traditional infrastructure.

The Moat of Long-Cycle Capital: The heavy-asset, long-duration development models once viewed as capital burdens are being redefined as "scarcity." The construction of hyperscale data centers and energy ecosystems requires immense capital thresholds and multi-cycle execution. By tapping public markets for large-scale, long-term capital, these firms build inimitable competitive moats, facilitating a valuation leap from "story-driven" to "asset-absorption-driven."

Risk & Outlook: Strategic Pivot to First Principles

Recent market performances of firms such as Arm and Astera Labs validate the capital market's strong preference for companies that solve tangible, structural problems. For enterprises in the IPO pipeline, the era of relying solely on an "AI label" has ended.

Strategic Outlook: Enterprises must evaluate their capacity to navigate underlying physical constraints and translate complex resources into systemic delivery solutions. Moving forward, firms with high capital absorption capacity and predictable output will continue to attract institutional favor amidst macro volatility. Conversely, pure technical narratives lacking physical underpinnings will face severe liquidity and valuation headwinds during the current "mean reversion" of market pricing.

Disclaimer:

Investment involves risk. The price of securities may go down as well as up, and past performance is not indicative of future results. This report is for informational purposes only and does not constitute investment advice.

https://www.ivy-service.com

- 1

- 2

- 3

- 4